If you are one of many storing corn this year, hoping for better prices later, you may now be wondering what you’ve gotten yourself into. After all, the fundamental outlook for grains as we near the end of 2015 is not so rosy.

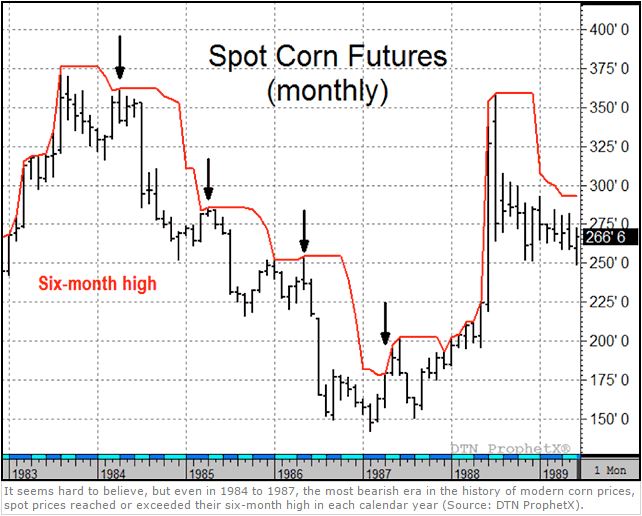

It seems hard to believe, but even in 1984 to 1987, the most bearish era in the history of modern corn prices, spot prices reached or exceeded their six-month high in each calendar year (Source: DTN ProphetX).

A second consecutive year of good growing weather has bulked up supplies of corn, soybeans, and wheat just as the U.S. dollar index is trading near its highest level in eight months. Cheaper currencies in Brazil and Ukraine along with plentiful supplies of feed wheat are hurting corn sales to the extent that total U.S. sales and shipments of corn are down 23% in 2015-16 from a year ago.

USDA’s U.S. ending corn stocks estimate of 13% for 2015-16 is a comfortable amount, but not as heavy as the 20% posted in 2000-01. I suspect that this year’s bearish concerns for corn are not so much about physical supplies as they are about the negative impacts of a strong U.S. dollar — a feature that was prominent in bear markets in both the mid-1980s and the late 1990s.

Given the above, I thought it would be helpful to go back and compare two exit strategies, taking special note of how they performed when corn’s fundamentals were bearish. The first strategy was to sell corn when the spot futures price reached or exceeded the high of the previous 12 months.

For our purposes, I simply wanted to know in how many calendar years since 1960 did spot corn futures reach or exceed the high of their previous 12 months at least once. And for years when the previous high was not reached, how long did that condition last? The idea behind the research is that prices commonly rotate from low to high, testing support and resistance along the way. If prices rotated to their one-year highs consistently enough, that would be valuable information for producers storing corn to know.

As it turned out, spot corn prices traded at or above their previous one-year high in 35 of the past 56 years, or 62% of the time. Not surprisingly, the longest stretch that prices missed reaching their one-year high covered the four calendar years from 1984 to 1987 when ending corn stocks hit their highest levels on record and saw an extreme bull market in the U.S. dollar peak in February 1985.

Clearly, waiting for a one-year high to sell stored corn during those four years would have been disastrous as prices eventually fell to their lowest levels in 15 years with exorbitant interest costs compounding the losses. In addition to the mid-1980s, there were two other periods that were also especially bearish: 1975 to 1977 and 1997 to 1999.

The strong U.S. dollar was an obvious factor in two of the three bearish periods, but the one commonality for all three was the return of corn to surplus after experiencing the bullishness of drought. The drought-inspired price peaks of 1974, 1983, and 1995-96 set up sharp declines in the following three to four years as weather conditions returned to normal. Until the bullishness of the previous drought was wrung out, prices would not hit their one-year rotations.

As bad as the idea of storing corn until prices hit their one-year high was, there is a second strategy that worked much better — even during years when corn’s fundamentals were bearish. Spot corn prices reached or exceeded their six-month high in 50 of the past 56 years, or 89% of the time.

Admittedly, in some years, corn prices only exceeded the previous six-month high by a tiny amount, but remarkably, six-month highs were exceeded in 1984, 1985, 1986, and 1987 — three of the most fundamentally bearish corn years on record. The longest stretch without hitting a six-month high was the two-year period of 1981 and 1982 — once again, a sharp decline that followed the drought of 1980.

It seems hard to believe, but even in 1984 to 1987, the most bearish era in the history of modern corn prices, spot prices reached or exceeded their six-month high in each calendar year (Source: DTN ProphetX).

In light of the evidence, the current situation in corn seems more understandable as we are now in the third year following the drought of 2012 and supplies are comfortable, but not excessive. Corn prices have dropped far enough to be unprofitable for many and have enticed commercials to turn net long 59,929 contracts in the futures market.

Of course, guarantees are never possible, but given corn’s past behavior, it seems highly probable that spot prices will rotate to at least their six-month high sometime in 2016, which is currently $4.38 3/4. The one-year high is currently the same price and is also a reasonable target for 2016 given the cheap price level that corn has already reached.

Do corn prices have to rotate to their six-month highs? For any specific year, the answer is no, they don’t. As we have seen, there are times when bearish pressures can be overwhelming.

However, in general, the answer is yes, they eventually do. Like inhaling after a long exhale, prices have to eventually offer advantages to both sides of the market to keep things functioning. In the long-run, the market has to work for consumers, commercials, and producers, and that is why prices have a strong tendency to rotate from low to high and back again. You simply can’t have a corn market without corn producers.

In times like this when corn prices are low, it is easy to get discouraged by the bearish outlook and succumb to the feeling that prices will never rebound. No one can say for sure when prices will trade higher again, but history favors the producer who understands the value of his or her corn and protects himself from the temptation to sell below cost. Good risk management can help you weather the storm, but the main requirement is understanding value — both corn’s and your own.

Todd Hultman can be reached at todd.hultman@dtn.com

Follow him on Twitter @ToddHultman1